Domestic banks are now in a virtuous cycle, looking forward to a particularly high performance in the three-year period 2023-2025, despite the difficulties recorded in the credit expansion part.

Spearheaded by the extremely favourable interest rate environment, banks are achieving strong revenue growth, high profitability - efficiency, while strengthening shareholder reward moves with dividend distributions and shares buyback, elements that act as a magnet for foreign investors.

The particularly positive climate for Greek banks was reflected yesterday at the Morgan Stanley conference in London, where the heads of the systemic banks spoke: Vassilis Psaltis (Alpha Bank), Fokion Karavias (Eurobank), Pavlos Mylonas (National Bank) and Christos Megalou (Piraeus Bank).

The investors in the context of the meetings held with the banks' staffs focused basically on 3 areas:

- Profitability - dividend policy. Banks underlined their estimate for dividend distribution for the fiscal year 2023, while they are also proceeding with buyback programs.

- Outlook for 2024. The outlook for the new year is particularly positive, as despite the gradual narrowing of the interest rate spread since the second quarter, the industry's profitability will remain high. Greece is expected to achieve growth rates significantly higher than in most euro area countries. Moreover, the country's strengths include political stability and Mitsotakis' commitment to accelerate reforms.

- Credit expansion and the difficulties recorded in generating new loans. For 2023, most banks will not "catch" the credit expansion target set in the budgets. Large repayments were noted, and the fact that 2023 was an election year had a negative impact. A significant acceleration in lending is expected in 2024 and 2025.

The key role of interest rates

Led by the favourable interest rate environment coupled with the growth momentum of the domestic economy, banks have already recorded a drastic improvement in metrics across all balance sheet lines since FY2022, with high interest income, strengthening fee income, a significant strengthening of the capital base and impressive return on tangible capital employed (RoTBV) ratios, dynamics that have acted as a magnet for attracting foreign institutional investors to domestic banks. Moreover, there does not seem to be a serious impact on the loan portfolio quality aspect.

Significantly, as reflected in the National Bank's placement prospectus, the bank expects core operating profit before provisions and after tax of over 1 billion per annum for the period 2023 - 2025. Eurobank, Piraeus Bank and Alpha Bank will also record similar dynamics, mutatis mutandis.

The dynamic growth of the sector and the prospects for the coming years were the catalyst for UniCredit's investment in Alpha Bank and the spectacular response of foreign institutional investors to the placement of National Bank.

As noted by the heads of domestic banks in London, the interest rate is close to its peak - most likely this will occur in the first quarter of 2024 - and will gradually decline (due to the increase in deposit rates), but will remain at very satisfactory levels due to the dominance of savings deposits. In addition, banks are moving to reinvest, at much better pricing, maturing assets that were at low yields.

The only dark spot is the difficulty in the credit expansion part, especially in the mortgage sector, and the failure to achieve the targets set, a weakness that is nevertheless offset by high interest rate profitability.

Banks are optimistic that from 2024 credit expansion rates will strengthen significantly, led by investment, where the Recovery Fund is making a decisive contribution, but also in retail banking, as a result of improving incomes and the booming property market.

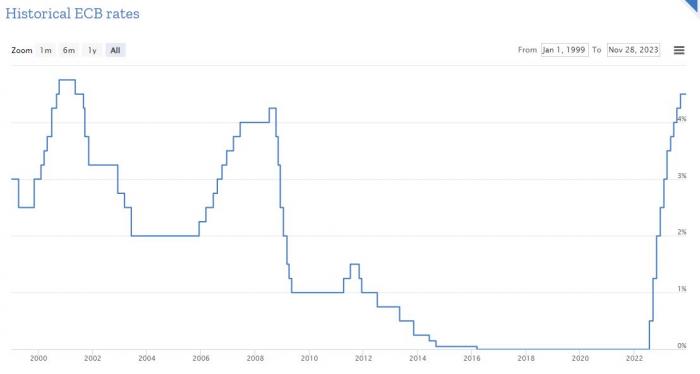

End of the era for zero interest rates

The ECB's sharp rise in interest rates has certainly caused and continues to cause jitters among businesses and households due to the rising cost of money, but the interest rate hike has ended an abnormal situation for banks and the economy: the maintenance of the euro's key interest rates at zero for too long. Zero interest rates for such a long period of time caused serious complications, the most serious of which was a spike in inflation.

It should be noted that in September 2014 the ECB lowered the key intervention rate to 0.05% which in early 2016 was reduced to the 0% level which was maintained until the summer of 2022.

The return of interest rates to normal levels restores the normal functioning of the banking system and dramatically boosts banks' interest income especially in Greece where the deposit structure, with the predominance of savings deposits (which have much lower interest rates than term deposits), allows banks to maximise the benefit of rising interest rates.

Even if the ECB proceeds with interest rate cuts from mid-2024, these will be modest and it is unlikely that we will return to a zero interest rate situation in the next few years.