What are Islamic banks? In western banking the interest rate reflects the remuneration that the depositor is entitled to and the price that the borrower would pay for utilising extra funds. Whether fixed or floating, interest rate is indirectly linked to the economy and the estimated economic performance of the financed venture. Within a financing situation the entrepreneur bears the business risk; he should ensure that cash flows meet the interest payments.

Collateral requirements and the contract itself are the bank’s cushions against business risk. Depositors normally do not bear any business risk as their remuneration is fixed too. Risk and reward are severed. Islamic banking adopts practices that are commensurate with the Islamic law. Perhaps the most well-known prohibition is that of interest; Islamic banks are neither allowed to charge nor receive it.

Instead to mobilise funds their financial products are either equity-based, where the bank and an entrepreneur enter a joint profit-sharing venture, or fee-based, where cost-plus-profit sales and leasing agreements are typical. Equity-based financing is perhaps the most distinctive feature compared to conventional banks, as it allows the sharing of risk and reward. For using funds beyond their means, the entrepreneurs commit to a profit-share ratio with the bank. Contrary to the interest rate case where the entrepreneur is always liable, here the remuneration is tied to the economic performance; hence the entrepreneur repays when the venture is profitable. No profits in a certain period (e.g., due to Covid-19); no repayment to the bank.

Such contracts are more demanding at the design stage, with solid business plans, stress-testing and reliable forecasting typically required. This heightens the importance of due diligence and monitoring, while it requires highly skilled personnel. Since profits are shared, the bank has strong incentives to ensure non-performing investments are minimal.

Equity-based contracts are also in place with the depositors, which are now quasi-investors. They receive a profit share ratio too, which is tied to the bank’s performance. If the bank is profitable, their reward is higher. If the bank’s investments turn sour then the remuneration to the depositors is reduced, or even zeroed. This is an effective mechanism to exert control on the bank. Depositors have the flexibility to withdraw their deposits from a mismanaged bank and place them with a profitable institution in search of higher reward. In fear of such behaviour bank managers have more incentives to work closely with the entrepreneur to ensure their investments remain profitable.

The choice of Islamic or conventional banking products falls entirely to the investor, although it is expected that investors from Muslim countries may show a preference to the former and even pay a premium. Yet, this selection per se may be informative to financial markets. For example, firms issuing Islamic financing attract a positive abnormal return in Saudi Arabia, suggesting that this move is welcomed by investors. The fact that Islamic banking products are built on the concept of risk, it has been found that they inspire a more responsible behavior; thus, mitigating credit risk.

How they compare to other financial institutions?

Islamic financial institutions have established their presence in the global financial system, with total assets under management of around $2.4 trillion, while maintaining a double-digit annual growth rate even amidst the financial crisis and political turmoil (IFSB, 2020). The comparative performance of Islamic banking has fuelled empirical research with important findings. Our collaborative research at UK and French academic institutions reveals that Islamic banking is not uniformly practiced across countries. Differences in product offerings and relative size of the Islamic banking sector are observed across the countries.

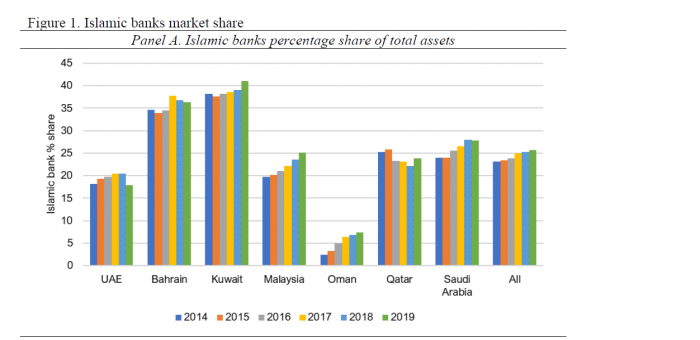

To keep the analysis tractable, we focus on countries where Islamic banking accounts for at least 5% of the total banking assets over the 2014-2019, to signify that it is an important feature of the country. The graph shows the evolution of the percentage share of Islamic banks within a sample of these countries based on Total Assets; a measure of bank size.

We observe that the share of Islamic banking is on an upward trend, and in 2019 is around 25% on average. In specific countries, like the UAE that the Prime Minister of Greece Kyriakos Mitsotakis recently visited, around 20% of the country’s deposits are placed with Islamic banks. Islamic finance is used to finance a wide variety of projects, from the purchase of aircraft - when Emirates acquires Airbuses - to the creation tourist complexes in the Gulf region. In Europe, the UK is home to four Islamic banks whose asset base is on a similar increasing trend (see Figure 1). Despite these representing less than 1% of the total assets in the UK banking system, the UK government has taken significant steps (e.g., legal and regulatory framework, issuance of a £200 million Islamic bond in 2014) to facilitate the operation of such alternative financial systems.

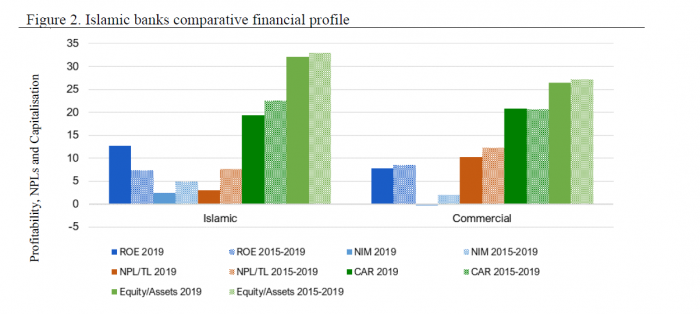

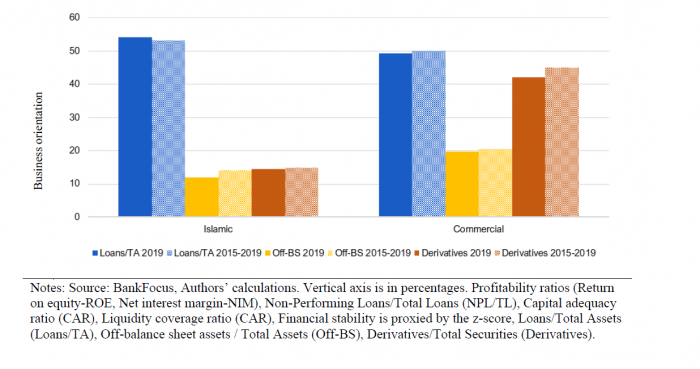

As far as the financial profile of Islamic banks is concerned, they are typically smaller than their conventional counterparts. They typically operate a relationship-based placing emphasis on maintaining long-term relationships with the customers; a behaviour that is mandated from the equity-based financial products. Securities investments are typically a lower fraction of the Islamic bank’s balance sheet, while they engage significantly less in high risk derivative trading and off-balance sheet practices (e.g., Loans/TA, Derivatives, Off-BS). To cope with the increased complexity of such contracts, Islamic banks invest in highly skilled personnel.

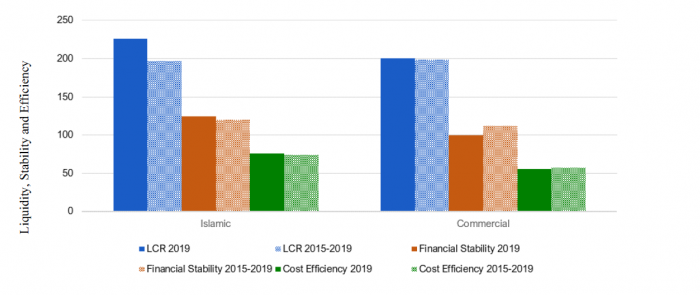

The higher required expertise and is typically reflected in their inferior cost efficiency metrics. By contrast, financial stability and credit risk measures are superior (e.g., NPLs), suggesting that their different approach in doing business has tangible merits. Liquidity risk management is challenging in Islamic banks due to the lack of an appropriate interbank market. For this reason, Islamic banks consciously operate at higher liquidity levels (e.g., Liquid Assets/TA, LCR). Due to the leverage restrictions stemming from their business model, Islamic banks tend to be better capitalised than their conventional counterparts.

Arguably Islamic banks operate outside of a strict profit-maximisation/cost-minimisation dogma, thereby focusing on social priorities and local development needs. Yet, their profitability ratios are comparable to those of conventional banks (e.g., ROEs). However, Islamic banks command significantly higher net interest margins, which suggests that they are better insulated against competitive pressure, as they instil a certain loyalty to customers who may be willing to go the extra mile for these services.

Why Islamic banking and finance may be important to Greece?

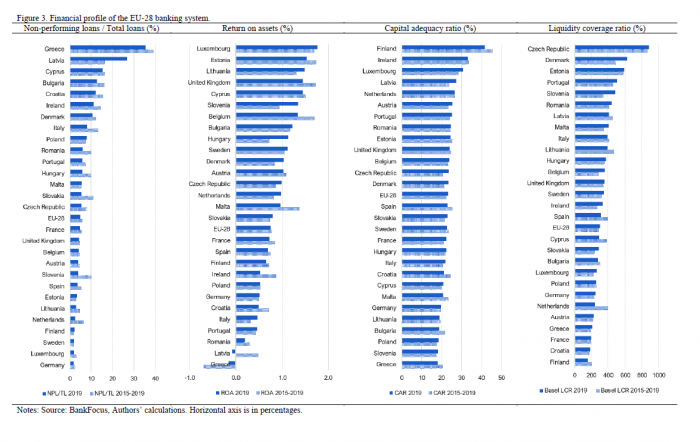

The Greek banking sector after several years of mismanagement and recapitalisations is trailing behind the EU-28 on several metrics. In the following section we present an overview of the comparative performance of the Greek banking sector over the 2015-2019 period with respect to the EU-28. A traditional sector that emphasizes on deposit-taking/loan-making business, the Greek banking sector has the highest NPLs in the EU-28 (NPL ratio), closely followed by Cyprus.

Bad loans of course have a detrimental impact on profitability, which over the examined period is negative; less so in 2019 (ROA). Despite the recapitalisations of the past years, Greek bank capitalisation is still the lowest (CAR) within the EU-28, although financial stability and liquidity (LCR) are comparable to most EU-28 banking systems and within safety limits. On this basis it appears that the Greek banking system is being held up. However, there are two indicators that are worthy of closer inspection.

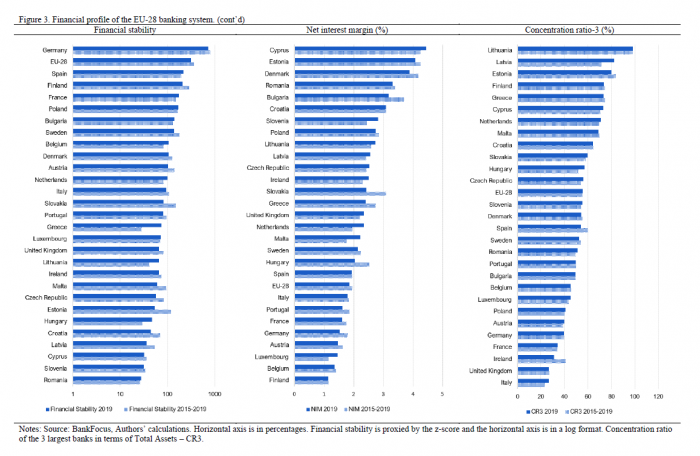

First, the net interest margin (NIM) indicator reflects the difference between the cost of funds (i.e., interest rates on deposits) and the revenues from lending (i.e., interest rates on loans). It is a measure of the pricing power that banks can command, directly related to their profitability. The paradox here is that Greek banks are trailing behind EU-28 in the mainstream profitability indicators (ROA, ROE); yet they appear to be performing better than many of their EU counterparts on the NIM basis. Assuming further that the cost of funds is close to zero due to the low interest rates in the EU, the NIM may be viewed as the cost of firm financing that Greek banks offer. Therefore, the relatively high NIM reflects that expensive funding is available to Greek firms.

Second, in terms of market structure, the Greek banking field is highly concentrated (CR3 ratio, HHI); thus, being similar to the newer members of the EU. This may not be a surprise as there are four systemic banks dominating the Greek banking sector. High concentration can be problematic as it deters financial innovation, it disincentivises banks to perfect their processes (i.e., the “quiet life” hypothesis), it increases financing costs and can ultimately deprive the economy from growing at its full potential.

Proposal

Against this background some steps should be taken to increase competition in the Greek banking sector. This would be beneficial for the thousands of extant Greek firms seeking financing, but it will also spur new start-ups. It would also properly incentivize the four systemic banks to achieve more. Allowing Islamic banks to operate in Greece, either individually or in cooperation with Greek banks as Islamic windows, may not have been timelier in terms of finance.

Further steps, including the issuance of an Islamic bond (Sukuk) and the introduction of Islamic equity indices in the Athens Stock Exchange may benefit further the financing of important national investments and promote the Greece’s economic recovery. (The London Stock Exchange can serve as a success story here with more than 50 billion US dollars for more than 65 Sukuk issues in 2018).

Finally, the geopolitical dynamics in our region may add to the successful implementation of such a project as the development of Islamic finance in Greece and the transformation of Greece as an Islamic financial hub in South East Mediterranean. The economic diplomacy of Greece with the UAE and Egypt may include in the agenda the possibility of the development of Islamic finance in Greece that may include the introduction of a combo of Islamic financial products like Islamic windows in cooperation with Greek banks, Sukuk bonds financing important projects in Greece and traded in the Athens Stock Exchange, as well as Islamic insurance services (Takaful) for the Islamic investments in Greece..

The views expressed in this article are personal

- Christos Alexakis is an Associate Professor at the ESC - Rennes School of Business. His work is published in academic journals, books and presented at international conferences. He has taught at the University of York, University of Leeds, University of Bradford, and University Cattolica in Milan as Visiting Professor, while he has held top management positions (CEO) in financial sector companies. During the period 2016-2020 was a member of the Stakeholders Group (SMSG) of the European Securities and Markets Authority (ESMA) and currently is the representative of the Bank of Greece in the Selection Panel of the Hellenic Financial Stability Fund (HFSF).

- Vasileios Pappas is an Associate Professor in Finance at the University of Kent. He is also deputy director in the GOLCER research center and visiting researcher at Lancaster University. His specialization is within empirical banking, Islamic finance and financial econometrics. His work is published in academic journals and presented at international conferences.

- Athina Petropoulou is a Post-doctoral Research Fellow at SOAS University of London. Her core research interests lie in the areas of banking, with a focus on credit risk, liquidity risk, efficiency and competition across alternative banking models.